Introduction

The Future of Affordable Auto Insurance is becoming a central concern for drivers worldwide. Rising repair costs, inflation, advanced vehicle technology, and increased accident severity have pushed premiums higher year after year. According to data from the Insurance Information Institute, auto insurance rates have risen significantly over the past decade, often outpacing wage growth.

As 2026 approaches, the auto insurance industry is undergoing a structural transformation. New technologies, regulatory changes, and shifting consumer behavior are redefining how risk is calculated and how premiums are priced. These changes are not only affecting insurers, they are reshaping what affordable coverage will look like in the near future.

This article explores the key trends shaping the future of affordable auto insurance in 2026, helping drivers identify where savings opportunities may emerge and how to prepare for a rapidly evolving insurance landscape.

1. Usage-Based Insurance Becomes the Standard

Usage-based insurance (UBI) is moving from niche to mainstream.

Rather than relying solely on demographic data and historical averages, UBI pricing uses real-world driving behavior, such as mileage, speed, braking patterns, and time of travel to determine premiums. Research highlighted by McKinsey & Company shows that UBI adoption is accelerating as insurers seek more accurate risk models.

By 2026, most major insurers are expected to offer some form of telematics-based policy.

Why this matters for affordability:

- Low-mileage drivers pay less

- Safe driving behavior is rewarded

- Remote and hybrid workers benefit

Drivers who actively manage their driving habits will gain greater control over insurance costs.

2. Artificial Intelligence Drives Fairer Pricing Models

Artificial intelligence is transforming underwriting and claims processing.

AI-driven analytics allow insurers to evaluate risk at a granular level, reducing reliance on broad assumptions. According to IBM, machine learning models improve pricing accuracy while reducing administrative costs.

As efficiency improves, insurers can pass savings on to customers, especially low-risk drivers who were previously overcharged.

Expected benefits by 2026:

- Faster and cheaper claims processing

- Reduced fraud-related losses

- More personalized premium calculations

Smarter pricing models mean fewer drivers subsidizing higher-risk profiles.

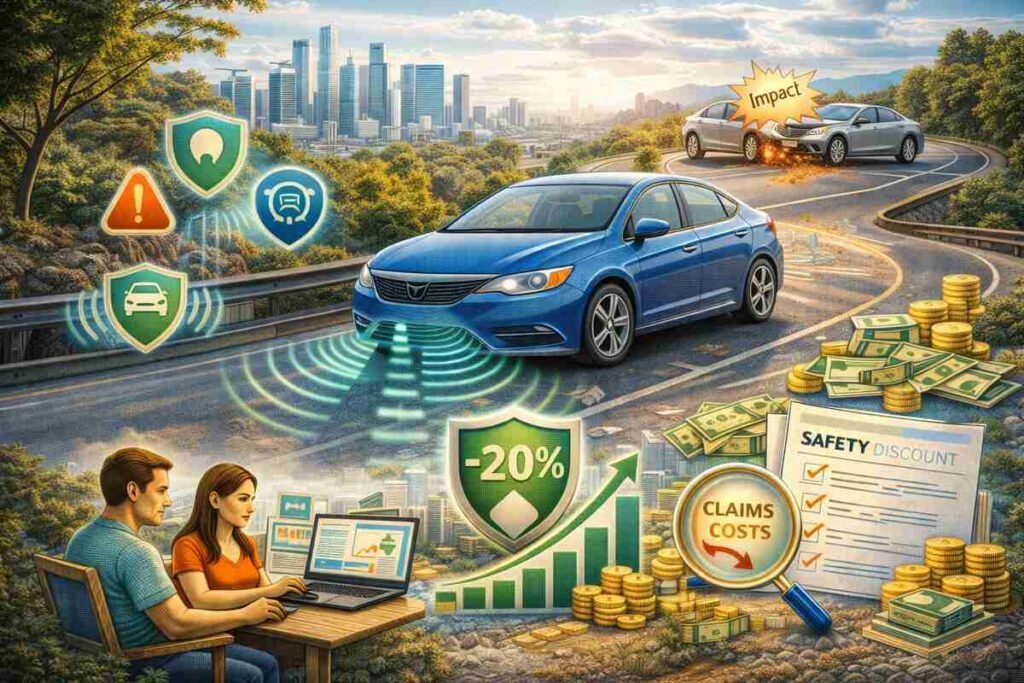

3. Vehicle Safety Technology Lowers Long-Term Premiums

Modern vehicles are increasingly equipped with advanced driver-assistance systems (ADAS), including automatic emergency braking, lane-keeping assistance, and adaptive cruise control.

Data analyzed by the National Highway Traffic Safety Administration shows that these technologies significantly reduce accident frequency and severity.

While advanced systems initially increase repair costs, insurers are recalibrating risk models as safety data improves.

Impact on affordability:

- Fewer accidents lead to lower claims costs

- Insurers expand safety-related discounts

- Long-term premium stabilization

By 2026, safety tech adoption is expected to be a net positive for insurance affordability.

4. Regulatory Pressure on Rate Transparency

Regulators are increasingly scrutinizing how insurers set prices.

In many regions, regulators are pushing for greater transparency around rating factors, algorithmic fairness, and consumer disclosures. Guidance from organizations like the National Association of Insurance Commissioners highlights a growing focus on equitable pricing.

Greater oversight limits excessive rate hikes and promotes competitive pricing.

What drivers can expect:

- Clearer explanations for premium increases

- Limits on discriminatory pricing factors

- Easier comparison between insurers

Transparency empowers consumers to shop smarter and avoid overpaying.

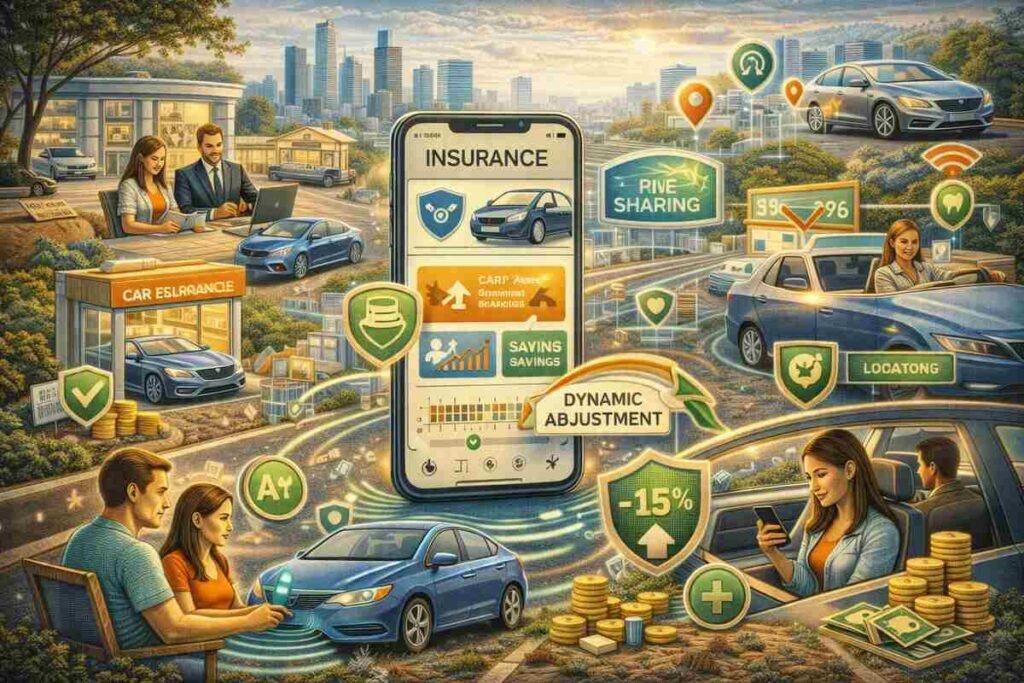

5. Embedded Insurance and Real-Time Policy Adjustments

Embedded insurance integrates coverage directly into digital platforms, such as car dealerships, ride-sharing apps, and vehicle subscription services.

Analysis from Deloitte indicates that embedded insurance reduces distribution costs and streamlines policy management.

By 2026, policies may adjust dynamically based on usage, location, or vehicle status.

Affordability advantages:

- Lower administrative overhead

- Flexible, short-term coverage options

- Real-time premium adjustments

This shift favors consumers who want tailored, pay-as-you-go coverage.

6. Credit-Based Pricing Faces Growing Limitations

Credit-based insurance scoring has long influenced premiums, particularly in the United States. However, consumer advocacy and regulatory scrutiny are reshaping its role.

Reports from the Federal Trade Commission acknowledge correlations between credit behavior and claims, but several states are now restricting or banning its use.

By 2026, insurers are expected to rely less on credit data and more on behavioral and vehicle-based metrics.

Why this improves affordability:

- Reduced penalties for financial hardship

- More accurate risk-based pricing

- Greater equity across income levels

This shift benefits drivers previously disadvantaged by credit-based models.

7. Electric Vehicles Reshape Insurance Economics

Electric vehicle (EV) adoption is accelerating, supported by government incentives and declining battery costs. According to the International Energy Agency, global EV sales continue to grow rapidly.

Initially, EV insurance was expensive due to high repair costs. However, insurers are adapting as data accumulates.

Trends affecting EV insurance costs:

- Improved repair networks

- Better parts availability

- Increased competition among insurers

By 2026, EV insurance premiums are expected to stabilize and in some cases undercut traditional vehicles.

8. Competition From Insurtech Startups

Insurtech companies are challenging traditional insurers with leaner operations, digital-first models, and customer-centric pricing.

Platforms highlighted by CB Insights demonstrate how automation and data-driven underwriting reduce overhead costs.

Increased competition forces legacy insurers to innovate and lower prices.

Consumer benefits include:

- Simplified policy management

- Faster claims settlements

- More transparent pricing

Competition remains one of the strongest drivers of affordability.

9. Consumer Behavior Becomes a Pricing Factor

Insurers are increasingly rewarding proactive risk management.

Defensive driving courses, vehicle maintenance tracking, and even real-time alerts can influence premiums. Research supported by AAA shows that driver education reduces accident likelihood.

By 2026, policyholders who actively engage with safety tools and education programs will see meaningful discounts.

What Drivers Can Do Now to Prepare

To benefit from future affordability trends, drivers should:

- Embrace telematics and safe driving programs

- Maintain accurate mileage reporting

- Stay informed about regulatory changes

- Compare insurers regularly

Preparation ensures access to the most competitive pricing models as they emerge.

Final Thoughts

The future of affordable auto insurance is data-driven, transparent, and increasingly personalized. While premiums may not universally decline, pricing accuracy and competition will create significant savings opportunities for informed drivers.

By understanding the trends shaping auto insurance in 2026, consumers can position themselves to benefit from innovation rather than absorb rising costs.

Affordable auto insurance is no longer about luck, it’s about alignment with how risk is measured in a smarter, fairer system.