A Quiet Revolution in Auto Insurance Is Saving Drivers Hundreds

Auto Coverage Benefits begin with putting safe drivers in control of their premiums through Usage-Based Insurance. If you’ve ever felt frustrated by paying high auto insurance rates despite careful driving, you’re not alone. For decades, insurers priced policies using broad factors like age, location, and vehicle type even though those rarely reflect how safely someone actually drives.

In 2025, that’s changing fast.

Usage-based insurance (UBI)—powered by telematics—uses real driving behavior to determine your premiums. It measures how smoothly you brake, when you drive, how far you travel, how quickly you accelerate, and more. Finally, your rate reflects who you are behind the wheel, not a demographic category.

According to a 2024 Harvard Business Review study, over 45% of U.S. drivers are expected to use a telematics-based insurance program by the end of 2025. And most early adopters are already seeing significant annual savings.

This guide explains how UBI works, why it’s transforming coverage, and how to take full advantage of it.

1. What Is Usage‑Based Insurance (Telematics)?

Usage‑based insurance is a pricing model that adjusts your premium according to real‑world driving behavior.

Telematics programs use data collected from:

- Smartphone apps

- Vehicle sensors

- Plug‑in devices

- Factory‑installed onboard systems

What Telematics Tracks

- Braking habits

- Cornering behavior

- Hard acceleration

- Speed consistency

- Nighttime driving

- Miles driven

Example:

A driver who avoids harsh braking and late‑night driving pays 20% less than someone with similar demographics but worse habits.

Research Insight: According to the Insurance Information Institute, telematics programs provide more accurate risk assessments and reward better driving performance.

Takeaway: UBI turns safe driving into real savings.

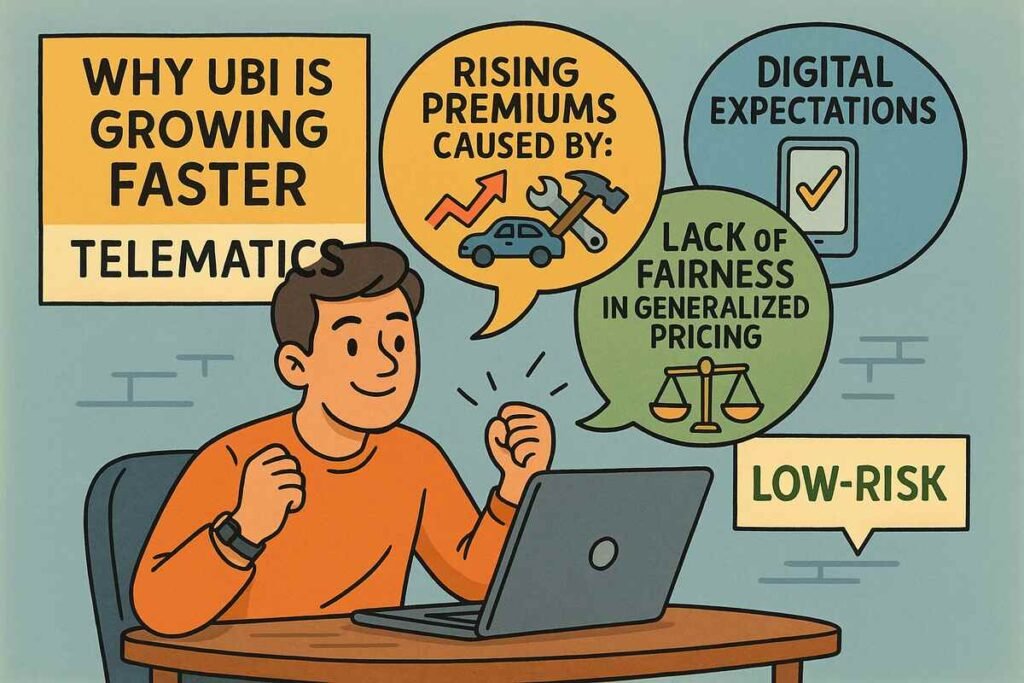

2. Why UBI Is Growing Faster Than Any Other Insurance Model

Best for: drivers frustrated with rising rates.

Telematics is expanding because it solves three major industry problems:

1. Rising premiums caused by:

- inflation

- costly repairs

- advanced vehicle tech

- expensive claims cycles

2. Lack of fairness in generalized pricing

Drivers want personalized rates.

3. Digital expectations

Consumers expect transparency and convenience.

Research Insight: A 2024 McKinsey mobility report found UBI policies may expand up to 400% worldwide by 2030, driven by safety‑data adoption and EV electrification.

Example:

A cautious driver frustrated with rate increases finally paid less after joining telematics because their driving data proved they were low‑risk.

Takeaway: UBI aligns cost with behavior not assumptions.

3. How Usage‑Based Insurance Actually Works

Once enrolled, drivers agree to share driving behavior in exchange for fairer pricing.

There Are Two Core Models

1. Pay‑How‑You‑Drive (PHYD)

Rates adjust based on behavior.

2. Pay‑Per‑Mile (PPM)

Pricing depends on mileage.

Best For:

- remote workers

- retirees

- city dwellers

- low‑mileage commuters

What Happens After Enrollment?

- you drive normally

- data is collected passively

- insurers score driving behavior

- pricing adjusts (monthly or at renewal)

Example:

Sarah reduced her annual mileage by 8,000 miles after shifting to remote work — her UBI program lowered her rate by $38/month.

Takeaway: Telematics makes price updates dynamic, not static.

4. Who Benefits Most From Usage‑Based Insurance?

Top Groups Who Save Big

- safe drivers

- infrequent drivers

- remote workers

- EV drivers

- city dwellers

- empty‑nest households

- drivers with clean records

Why Savings Are Higher

Telematics removes risk‑assumptions.

Example:

An older driver with perfect habits might finally pay less than a teenager with poor driving patterns.

Research Insight: A 2024 Forbes Advisor automotive insurance analysis found telematics programs reduce premiums between 15% and 35% for qualifying drivers.

5. Pros & Cons of UBI Programs

Pros

- Personalized pricing

- More control over premiums

- Rewards safe habits

- Encourages better driving

- Transparent data

Cons

- Privacy concerns for some drivers

- Nighttime driving can raise rates

- Hard braking may affect scores

Research Insight: The Cleveland Clinic reports technology‑assisted driving improves long‑term safety habits.

Takeaway: Understanding data sensitivity helps you control the outcome.

6. The Best Usage‑Based Programs in 2025

Progressive Snapshot

How it works: monitors braking & acceleration.

https://www.progressive.com/auto/discounts/snapshot/

Allstate Drivewise

How it works: offers score transparency and rewards.

https://www.allstate.com/drivewise

GEICO DriveEasy

How it works: uses smartphone telematics for ongoing savings.

https://www.geico.com/save/driveeasy/

State Farm Drive Safe & Save

Ideal for: low‑mileage drivers.

https://www.statefarm.com/insurance/auto/discounts/drive-safe-save

Takeaway: Competition is driving consumer‑friendly innovation.

Real Driver Example: $820 Saved in One Year

David, a remote engineer, drove less than 5,500 miles in 2024.

He switched to pay‑per‑mile telematics.

Annual savings: $820

Lesson: driving less = spending less.

Comparison Table: Telematics vs Traditional Insurance

| Feature | Telematics (UBI) | Traditional Insurance |

|---|---|---|

| Pricing | Behavior‑based | Demographic‑based |

| Savings Potential | High | Limited |

| Transparency | Strong | Weak |

| Best For | Safe & low‑mileage drivers | Average drivers |

| Data Required | Yes | Minimal |

Frequently Asked Questions About Usage‑Based Insurance

1. Can UBI programs raise my rates?

Yes, if driving patterns are risky.

2. How long does tracking last?

Most programs track continuously.

3. Does UBI work with EVs?

Increasingly yes, especially with integrated software.

4. Is phone‑based tracking accurate?

Generally yes, but results vary by platform.

5. Can I switch back to traditional insurance?

Absolutely anytime.

Final Thoughts: Auto Coverage Benefits

Usage‑based insurance is reshaping auto coverage permanently. It rewards safe drivers, lowers costs for low‑mileage households, and uses technology to make pricing fairer than ever.

If you want lower premiums in 2025, UBI is one of the smartest paths available.

If this guide helped you understand usage‑based insurance, share it and explore more savings strategies on our blog.