Car Insurance Scams Are Evolving and Drivers Must Stay Ahead

Car insurance fraud isn’t just a problem for insurers, it directly affects your premiums, your claims, and your financial security. As insurance systems become more digital and connected in 2026, scammers are getting smarter, faster, and more convincing.

From staged accidents and fake repair shops to phishing emails and AI-generated calls, modern insurance scams are harder to detect than ever. According to the National Insurance Crime Bureau (NICB), insurance fraud costs drivers billions each year, adding hundreds of dollars annually to the average premium.

This in-depth FAQ guide explains how car insurance fraud works in 2026, the most common scams targeting drivers, and most importantly how you can protect yourself with confidence.

What Is Car Insurance Fraud?

Car insurance fraud occurs when someone deliberately deceives an insurer for financial gain. Fraud can be committed by criminals, organized rings, repair shops, or even other drivers.

Two Main Types of Fraud

- Hard fraud: Intentional acts like staged accidents or fake injuries

- Soft fraud: Exaggerating damages, inflating claims, or misrepresenting facts

Reference: The National Insurance Crime Bureau provides ongoing updates on auto insurance fraud trends.

Takeaway: Even “small lies” can count as fraud and raise your rates.

Why Fraud Is Increasing in 2026

Several trends are driving the rise in car insurance fraud.

Key Factors

- More online claims and digital communication

- AI-generated phishing and deepfake calls

- Rising repair and medical costs

- Increased vehicle technology complexity

- Cross-border and organized fraud rings

Example: Scammers now impersonate insurers using realistic emails and AI voice messages.

Reference: The Federal Trade Commission reports a sharp increase in impersonation scams involving insurance providers.

Takeaway: Digital convenience requires digital awareness.

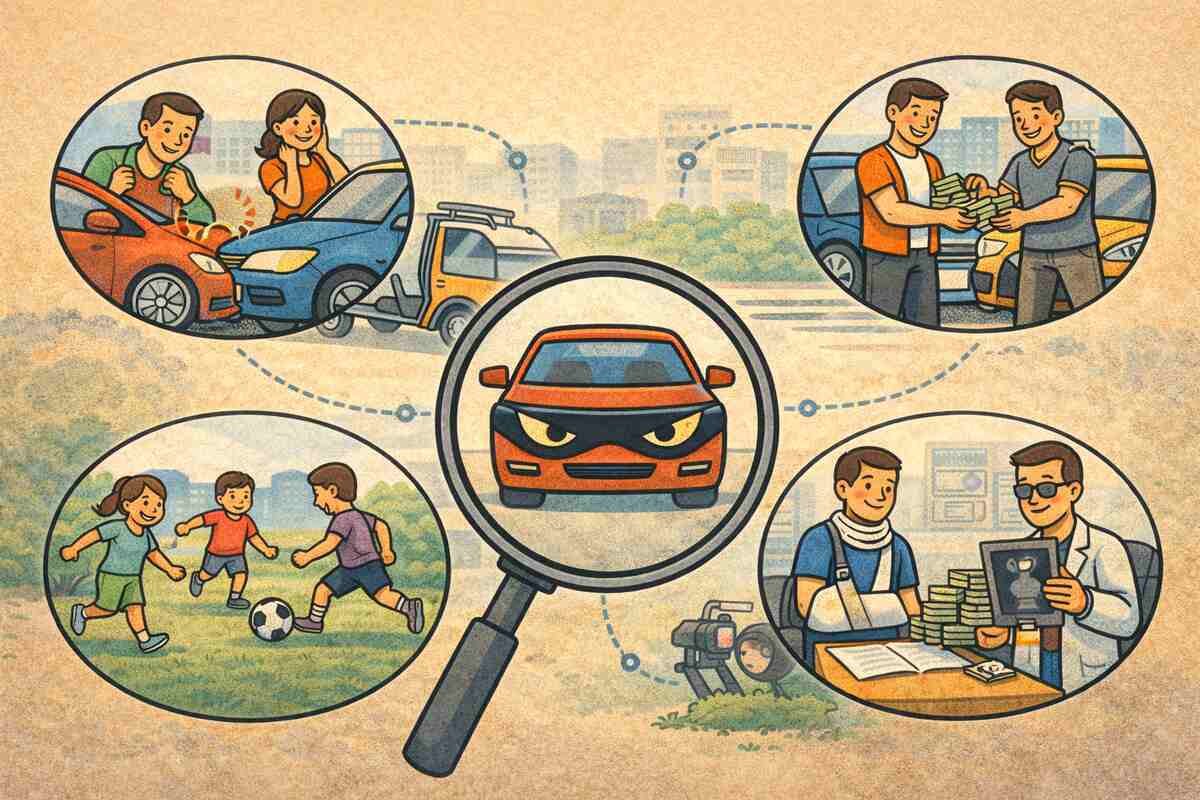

1. Staged Accident Scams

One of the most dangerous and costly types of insurance fraud.

How It Works

- Fraudsters deliberately cause or fake an accident

- Innocent drivers are blamed

- Fake witnesses and injuries are reported

Warning Signs

- Sudden stops with no reason

- Multiple passengers claiming injury

- Pressure to avoid police involvement

Example: A driver is brake-checked at low speed, then accused of rear-ending.

Protection Tip: Always call the police after an accident.

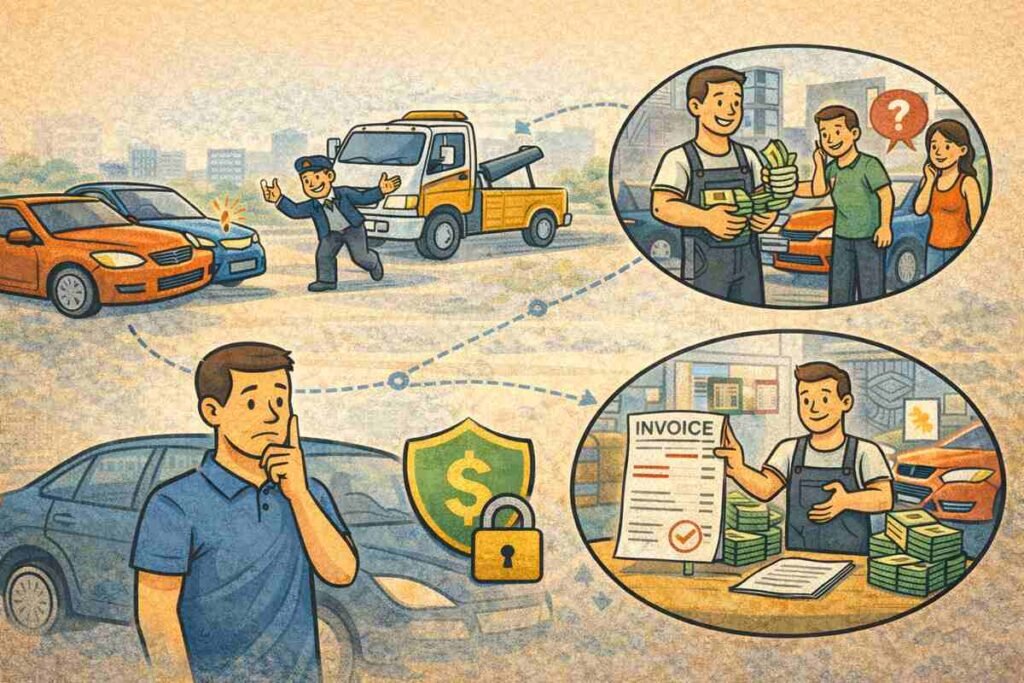

2. Fake Repair Shop & Tow Truck Scams

After accidents, scammers move quickly.

How It Works

- Tow trucks arrive unrequested

- Drivers are pressured to use specific repair shops

- Repairs are inflated or unnecessary

Reference: The NICB warns about predatory towing operations.

Protection Tip: Use insurer-approved repair facilities.

3. Phishing Emails & Fake Insurance Calls

Technology has made impersonation frighteningly realistic.

Common Tactics

- Emails claiming “policy cancellation”

- Texts requesting immediate payment

- AI-generated phone calls mimicking agents

Example: A fake email directs you to a lookalike payment portal.

Reference: The FTC phishing guidance explains how scammers mimic legitimate companies.

Protection Tip: Never click links log in directly to your insurer’s official site.

4. Medical Billing & Injury Fraud

Some scams exploit post-accident stress.

How It Works

- Fake clinics bill insurers for treatments you never received

- Exaggerated injury claims are filed in your name

Warning Sign: You receive medical bills without treatment.

Protection Tip: Review all Explanation of Benefits (EOBs).

5. Policy Application Fraud (Rate Manipulation)

Sometimes fraud happens before a policy even begins.

Examples

- Lying about garaging address

- Misstating mileage

- Hiding additional drivers

Consequence: Claims can be denied—even years later.

Protection Tip: Always provide accurate information.

6. Digital Claim Manipulation & Photo Fraud

AI editing tools have introduced new risks.

How It Works

- Photos are altered to exaggerate damage

- Old accident images are reused

Insurer Response: AI fraud detection systems flag inconsistencies.

Protection Tip: Take real-time photos with timestamps.

7. How Insurers Detect Fraud in 2026

Insurance companies now use advanced technology.

Fraud Detection Tools

- AI pattern recognition

- Telematics and crash data

- Cross-claim databases

- Repair cost benchmarking

Reference: Forbes Advisor explains how insurers use analytics to stop fraud.

Takeaway: Fraud is harder to get away with than ever.

What To Do If You Suspect Insurance Fraud

Immediate Steps

- Document everything

- Contact your insurer directly

- File a police report if needed

- Report fraud to NICB or FTC

Takeaway: Early reporting protects you.

Real-Life Example: A Driver Who Avoided a Scam

After a minor accident, Emma was approached by a tow truck she didn’t call. She refused, contacted her insurer, and avoided thousands in fraudulent charges.

Lesson: Slowing down prevents costly mistakes.

Comparison Table: Legitimate Claims vs Fraud Red Flags

| Legitimate Claim | Fraud Warning Sign |

|---|---|

| Police report filed | Pressure to avoid police |

| Insurer communication | Unsolicited calls |

| Clear documentation | Conflicting stories |

| Approved repair shops | Pushy tow operators |

Frequently Asked Questions About Car Insurance Fraud (2026)

1. Can fraud raise my premiums even if I’m innocent?

Yes—area-wide fraud increases rates.

2. Should I report suspected fraud?

Absolutely—it protects everyone.

3. Are digital claims safe?

Yes, when using official insurer platforms.

4. Can scammers use my identity?

Yes—monitor your credit and EOBs.

5. What’s the safest way to file a claim?

Through your insurer’s official app or portal.

Final Thoughts

Car insurance fraud in 2026 is more sophisticated but so are the tools to fight it. By staying informed, slowing down after accidents, and using official digital channels, you protect yourself from scams that could cost thousands.

If this guide helped you feel more confident about fraud prevention, share it or explore more smart insurance resources on our blog.